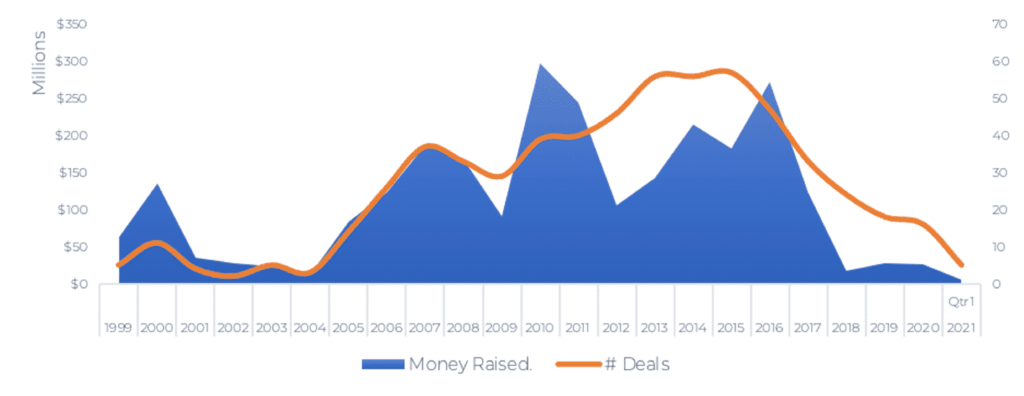

Going back between 2006 and 2017, hundreds of ad networks and dozens of DSPs, SSPs, exchanges, anti-fraud solutions, attribution solutions, and other companies were able to raise billions of dollars in the digital marketing ecosystem. Even if you look at 2015 LUMAscape, you would see one thousand logos, and adtech investments have decreased in number and size over the last decade (graph from Crunchbase).

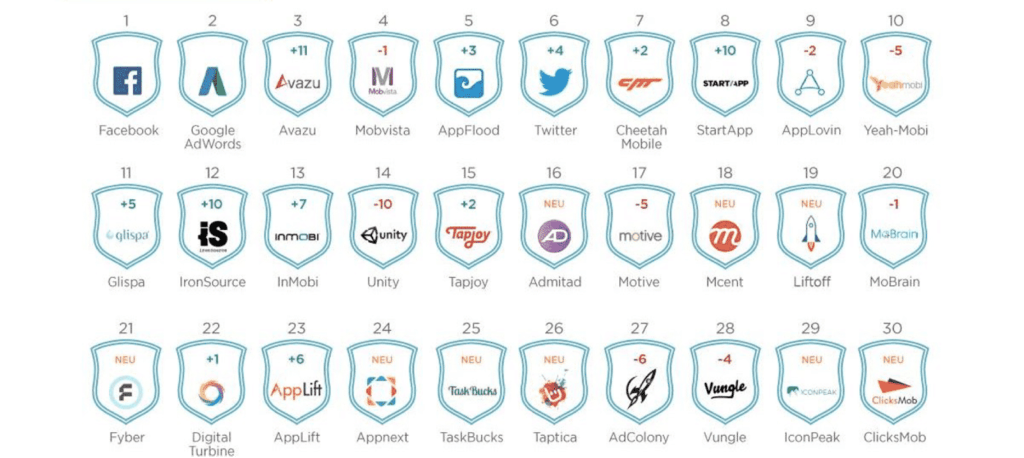

If we look at the 2016 Appsflyer Performance Index Global Power Ranking, we faced a very different landscape. In 2021 it would be a tableau that would interest a marketer.

The beginning of the pandemic in 2020 opened the doors of a world where many industries have become even more digital. If we think of 2020 as a year in which this transformation started and was built, then 2021 was a year in which the digital industry was grounded. Adtech companies quickly took steps in many areas of digital and became giants.

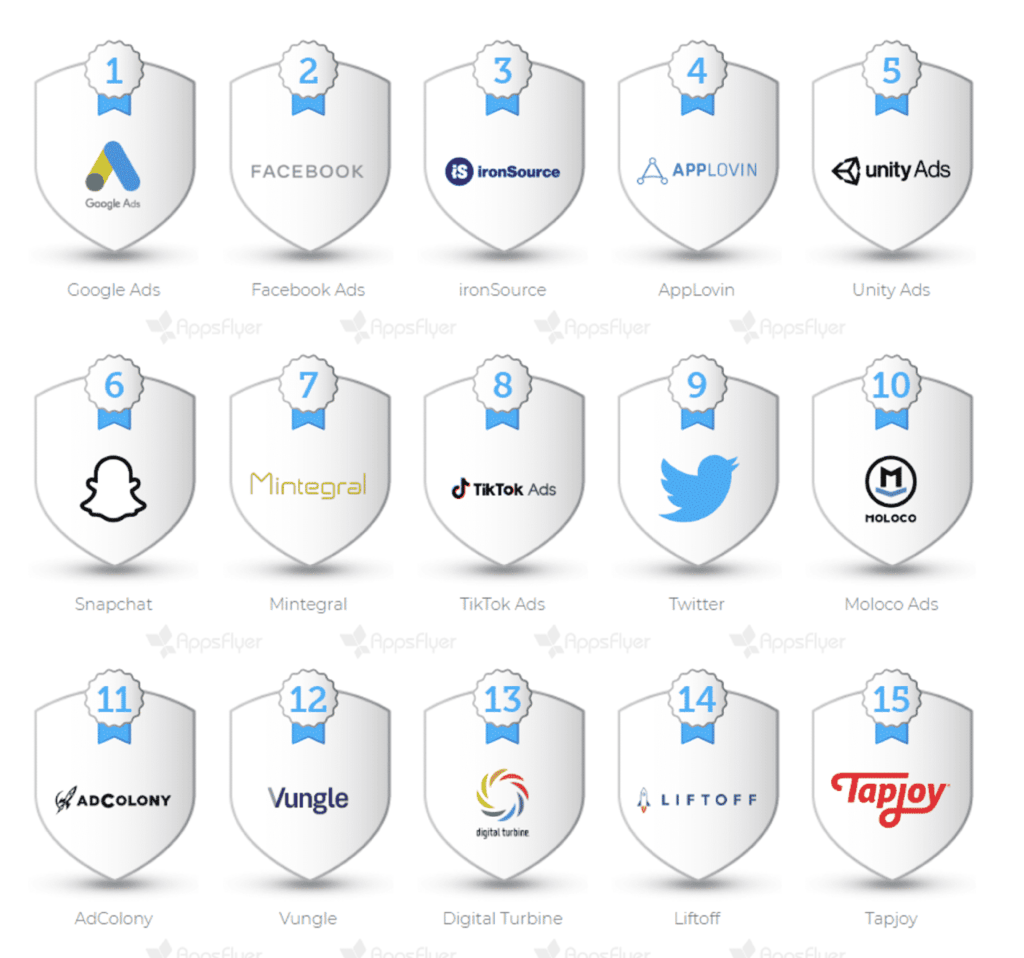

Now, the 2020 Appsflyer index shows a very different image.

In addition to Appsflyer, you can check out Adjust’s Top Ranked Adtech companies here.

In this article, you will find the answer to why the giant adtech companies and ad networks in the industry are taking steps to get a larger share of the adtech pie.

What was the main reason behind this transformation? We can easily say Killing IDFA (not exactly killing) and SKAdnetwork made an impact. Top of the walled gardens (you know who they are) saw some decline in their mobile user acquisition market share, and as a matter of course, Apple Search Ads had a massive increase on the market. However,it wasn’t just ASA that increased its share in this pie. While Google and Facebook were reacting slowly, other ad networks took action quickly. Some adopted SKAdnetwork, while others continued to insist on alternative attribution models, which is device fingerprinting.

Of course, the other reason was the pandemic. The last year has been extraordinary. Governments throughout the world reacted in the same way–putting their citizens on lockdown. In just one year, most of the mobile verticals, such as e-Commerce, gaming, and social media, experienced the equivalent of a 10-year growth. All indications point to this growth continuing once the lockdowns are lifted.

When we look at the history of Mobile Marketing, it is obvious many innovations and new capabilities that are focused on advertising and monetization have emerged. These capabilities include:

- Ad network (s side, demand side, retargeting and remarketing, and on-device preload platforms)

- Ad exchange

- Mediation

- Measurement

- Marketing Intelligence

- Analytics and Optimization Tools

- Ads Automation (bids, campaigns, and placements)

- Agency (creative and campaign management)

When we look at Mobile Lumascape, we see there are so many players in the area which cover at least one of these capabilities. However, this article will focus on the titans.

Adtech Giants

In 2021, many of the formerly mid-tier user acquisition partners saw market share growth. Here are five of the most important ones, SDK networks, and a discussion of what each one has to offer.

Ironsource

Upopa

Following the acquisition of Upopa, the Upopa founders joined ironSource’s internal innovation lab, ironLabs, which is focused on developing new products. According to ironSource, the innovation lab allows for the rapid development of new applications for numerous platforms.The acquisition of Upopa allows for the inclusion of expertise in mobile game development in the company’s current offerings.

Soomla

Soomla’s ad-quality insights are available as a software-as-a-service (SaaS) solution to assist developers in managing ads that run within their apps. Ads that are misleading or violate a “deny list,” for example, may negatively impact the user experience and result in churn (people deciding to drop an app or game). Developers can use such information to improve the user experience.

The goal, according to the co-founder of Ironsource, is to become a full platform for mobile app developers, with new capabilities that will enable developers to build, grow, and sustain profitable and successful enterprises.

Lunalabs

Creatives are a vital element of creating a great user experience, and their role has only grown in importance as the battle for user attention heats up. But developing and testing ad creatives at scale is extremely tough and expensive. Luna Labs solves this problem by providing app developers with high-quality end-to-end ad creation management.

Tapjoy

The acquisition of Tapjoy is expected to strengthen the ironSource platform offering for mobile app and game developers through several areas of synergy; ironSource customers will be able to generate more revenue with greater access to diversified advertiser demand, including through the Tapjoy marketplace. Customers will also gain access to complementary technology that will help app developers enhance their in-game economies. The acquisition will expand ironSource’s SDK presence across both applications and games, increasing the company’s market scale.

Bidalgo

IronSource claims the acquisition will enable it to offer a broader range of marketing-focused products, enhancing the platform’s power and value for app marketers (when combined with its current creative management solution, Luna Labs). Bidalgo’s customer base in apps beyond games, who use Bidalgo’s technology to manage and optimize their marketing expenditure inthe leading social, dating, and e-Commerce apps,, will enable ironSource to deepen its market presence across the entire app economy.

Vungle

Vungle + Liftoff

The joining of two industry titans is a once-in-a-lifetime event. This combination will help both firms accelerate major growth projects and enable them to continue to provide world-class solutions to the industry, fuelled by market-leading products and technical innovations.

Algolift

After Apple’s decision to deprecate the IDFA, Vungle’s acquisition of AlgoLift is the most exciting news in the mobile advertising sector. AlgoLift was one of the most well-positioned startups to deal with the industry’s shift away from device identifiers and toward probabilistic and inferential targeting. Vungle is strengthening its position in the emerging non-deterministic, privacy-centric advertising landscape by acquiring AlgoLift. They will be well-positioned as the mobile advertising market undergoes this privacy-centric development, due to AlgoLift’s measurement models and probabilistic attribution approaches.

GameRefinery

Vungle Creative Labs (VCL) will take advantage of GameRefinery’s image recognition and creative tagging capabilities. VCL’s considerable experience in cutting-edge creative and UA, combined with granular data on visual variables such as styles and genre fit, allows it to give industry-leading performance recommendations for its most important clients.

Both companies are aligned with what mobile game creators are seeking, and their coming together means they will have access to an arsenal of tools that will help them to grow even more in a post-IDFA, contextual environment.

Jetfuel

JetFuel automates campaign planning and execution, eliminating the time-consuming manual labor associated with traditional influencer marketing. Advertisers are charged on a cost-per-action (CPA) basis, guaranteeing they get measurable results with a high return on investment. JetFuel empowers influencers to generate real, unique promotions that produce results because they know their audience best and are specialists at creating viral content leading viewers to action.

As influencers become a more scaled and engaging way for mobile audiences to discover and connect with app content, they will become increasingly important. Vungle and JetFuel have teamed up to create a new gateway for digital entrepreneurs of all sizes throughout the world, combining Vungle’s knowledge of user acquisition with JetFuel’s expertise in social media and influencer marketing.

TreSensa

Vungle Creative Labs’ solution from TreSensa allows them to share their experience with their partners via platform-based creative technology, as well as provide data insights and recommendations at scale. Advertisers using Vungle will get access to a new suite of immediate playables, as well as additional services for Pro and Enterprise SaaS users and the option to export the creatives for use across all key platforms and channels.

Applovin

Adjust

With the help of the acquisition of Adjust, Applovin’s wholly-owned Adjust property has access to that aggregated data, and it is only used for serving ads within Applovin’s first-party ecosystem of games. It appears unlikely that Applovin would be barred from using Adjust to probabilistically attribute users when cross-promoting them between apps. Applovin would no longer need to publish all of its apps from the same App Store account, which is essential to use the IDFV as a single identification.

Mopub

Applovin’s acquisition of MoPub helps it achieve the goal of acquiring engaged users by giving its SDK access to MoPub’s existing publisher client base, eliminating a significant supply competitor and giving its demand platform, AppDiscovery, a competitive advantage. According to Applovin’s blog post on the acquisition, MoPub will be shut down and current MoPub users will be transferred to Applovin’s platform. Every impression filled on behalf of publisher customers is tracked by supply platforms: bid levels, fill rates, and so on. Applovin obtains this data in real-time through an in-app bidding platform like MAX and can aggregate it in ways that benefit all elements of its business, which is especially useful in the post-ATT context.

Given that practically all other mobile advertising systems have both a demand and supply component and most are constructing bidding (mediation) solutions, MoPub may have been the final actual supply provider available for acquisition. As with Applovin’s purchase of Adjust, a variety of justifications can be offered: corporate salesforce, access to non-gaming merchandise, and SDK footprint. However, like with Adjust, I don’t believe any of these reasons explain it. It’s more likely that Applovin now has access to a massive quantity of inventory supply as a result of its acquisition of MoPub, which has a beneficial impact on the rest of the company.

Lion Studios & Machine Zone

It would be impossible not to mention the gaming vertical, which constitutes an important part of the mobile market share. With the help of the acquisition of Lion Studios and Machine Zone, Applovin aims to assist mobile app developers in publishing, promoting, and getting their apps discovered. Thushus advancing its efforts to build a larger and more resilient independent app ecosystem said AppLovin’s CEO.

Digital Turbine

Fyber

Fyber is made up of three components that work together and have a specific purpose for a broader adtech strategy.The first is their expanding exchange. Then there’s mediation, which is a smaller part of their company but is developing quickly. It will assist the publishers’ Digital Turbine preload onto devices with monetization management. The final feature is their offer wall. Although this is a historical business, they consider the opportunity to cross-promote and recommend apps, content, and services to the telecoms they work with to be a benefit.

Adcolony

Another acquisition made by Digital Turbine was Adcolony. Adcolony brings with it a big SDK footprint, along with many complementary and additive solutions.

Appreciate

The acquisition of Appreciate is in line with Digital Turbine’s stated aim of providing a holistic media and advertising solution for the operator and OEM partners, as well as improving end users’ mobile experiences by bringing highly relevant content to their fingertips.

Unityads

Playnomics

Playnomics developed an algorithm to anticipate how anonymous players will behave, including who is likely to spend money, who should be targeted with promotions, and who the developer should pay attention to in order to avoid the dreaded churn (or the decision to stop playing a game). To put the data into action, Playnomics developed tailored marketing for mobile apps and games. Considering these capabilities, acquisition of Playnomics is a strategy of Unity to become an adtech giant.

Everplay

Everyplay allows players to post instant replay footage of their most amazing, entertaining, ridiculous, or embarrassing moments, allowing loyal fans to evangelize your game and spread the word to others. Instant replay revolutionized sports broadcasting, and it is now revolutionizing gaming as well.

Gameads

GameAds is a video ad-sharing tool that helps game developers locate new customers interested in playing their games and monetize non-paying players with video advertising. While Everyplay and GameAds are both set to be integrated into Unity to make them even more accessible, games and developers working with other engines are urged to use the services and take advantage of the most engaging user acquisition methods available. These services will work in tandem with Unity Cloud, Unity’s cross-promotion ad-sharing network, which is still in early stages of development. It provides elegantly complementing ways to reach a quality audience.

Zynga & Chartboost

So far, we have focused on the steps taken by adnetworks to become adtech giants. We mentioned that acquiring game companies is actually another important strategy on this path. But what if a game company acquires an ad network? Zynga operates a portfolio of 30 games, and of course, a game company with such a wide product range is looking for efficiency. Zynga’s recent hypercasual M&A activity, which included the acquisitions of Rollic and Oncosoft, demonstrates the significance of in-game ad inventory, both in terms of cross-promoting its games and earning additional money. In addition, regardless of the modifications made by Apple and IDFA, effective digital businesses require their own adtech solutions. This has implications for the Chartboost acquisition.

Final Thoughts

We don’t know who will win this race. Maybe there won’t be a single winner. However, one thing is certain, adtech companies in the shadow of Facebook and Google have staged a great attack in the last few years.

Adtech giants can’t collect data like they used to do, and their capacities are likely to be severely limited in the future due to privacy concerns. As they concentrate consumer touchpoints and first-party mobile user experiences, they position themselves for better targeting and performance.

Could not generate text at this time.

The rise of giant adtech companies in 2021 marked a pivotal moment in the digital marketing landscape, as the industry evolved to meet the demands of a world that had gone almost entirely online. The pandemic accelerated the shift toward digital-first strategies, and adtech players adapted swiftly, leveraging advanced machine learning, privacy-compliant solutions, and omnichannel capabilities to stay ahead. Platforms such as Google Ads, The Trade Desk, and Facebook Ads emerged as dominant forces, redefining how marketers approached targeting, measurement, and engagement. Meanwhile, smaller players consolidated or pivoted into niche markets to survive the fierce competition. The result? A streamlined ecosystem where the biggest names wielded unparalleled influence, but innovation still thrived in pockets of specialization. As we look back

By 2021, the adtech landscape had transformed into a battleground dominated by a handful of giants, each vying for supremacy in a digital-first world. The pandemic accelerated the shift, pushing brands and businesses to double down on their online strategies, giving adtech companies the perfect storm to innovate and expand. Platforms like Google Ads and Facebook Ads cemented their positions at the top, while rising stars like TikTok Ads and programmatic powerhouses carved out their share of the pie. Meanwhile, tools like Appsflyer and Adjust became indispensable for marketers aiming to navigate the complex web of attribution, fraud prevention, and campaign optimization. These giants didn’t just grow; they evolved, investing heavily in AI, machine learning, and privacy-first solutions